Please Follow us on Gab, Minds, Telegram, Rumble, Gab TV, GETTR

Reprinted with permission Mises Institute Thorsten Polleit

Speaking at the Jackson Hole meeting on August 27, 2021, Federal Reserve (Fed) chairman Jerome J. Powell indicated that he supported “tapering” toward the end of this year and hastened to add that interest rate hikes are still a long way off. The term “tapering” means that the central bank reduces its monthly purchases of bonds and slows down the monthly increase in the quantity of money accordingly. In other words, even with tapering, the Fed will still churn out newly printed US dollar balances, but to a lesser extent than before; that is, it will still cause monetary inflation, but less than before.

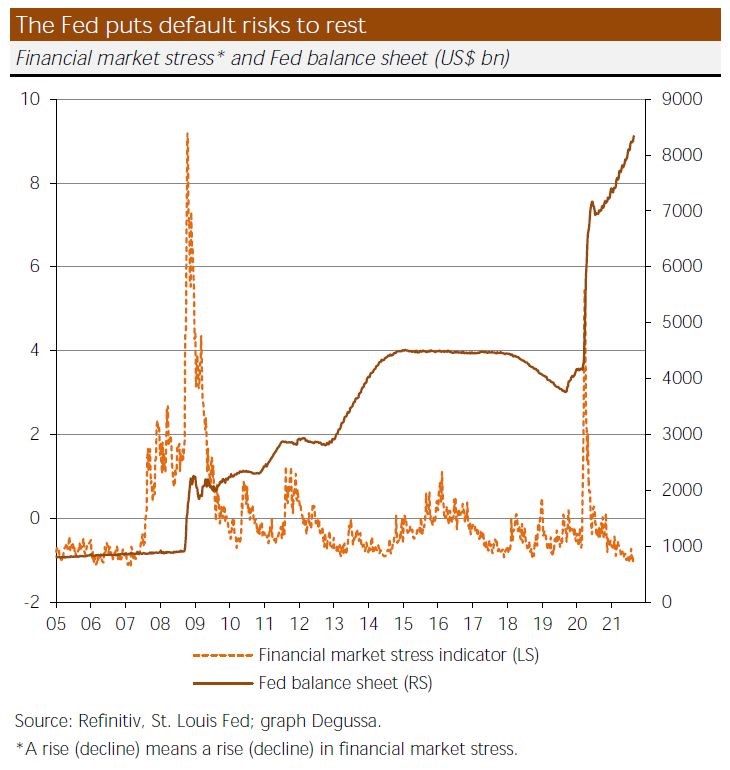

Financial markets were not alarmed by the Fed’s announcement that it might take its foot off the accelerator pedal a little: ten-year US Treasury yields are still trading at a relatively low level of 1.3 percent, the S&P 500 stock index hovers around record highs. Could it be that investors do not believe in the Fed’s suggestion that tapering will begin soon? Or is tapering of much lower importance for financial market asset prices and economic activity going forward than we think? Well, I believe the second question nails it. To understand this, we need to point out that the Fed has put a “safety net” under financial markets.

As a result of the politically dictated lockdown crisis in early 2020, investors feared a collapse of the economic and financial system. Credit markets, in particular, went wild. Borrowing costs skyrocketed as risk premiums rose drastically. Market liquidity dried up, putting great pressure on borrowers in need of funding. It wasn’t long before the Fed said it would underwrite the credit market, that it would open the monetary spigots and issue all the money needed to fund government agencies, banks, hedge funds, and businesses. The Fed’s announcement did what it was supposed to do: credit markets calmed down. Credit started flowing again; system failure was prevented.

In fact, the Fed’s creation of a safety net is nothing new. It is perhaps better known as the “Greenspan put.” During the 1987 stock market crash, then Fed chairman Alan Greenspan lowered interest rates drastically to help stock prices recover—and thus set a precedent that the Fed would come to rescue in financial crises. (The term “put” describes an option which gives its holder the right, but not the obligation, to sell the underlying asset at a predetermined price within a specified time frame. However, the term “safety net” might be more appropriate than “put” in this context, as investors don’t have to pay for the Fed’s support and fear an expiry date.)

The truth is that the US dollar fiat money system now depends more than ever on the Fed to provide commercial banks with sufficient base money. Given the excessively high level of debt in the system, the Fed must also do its best to keep market interest rates artificially low. To achieve this, the Fed can lower its short-term funding rate, which determines banks’ funding costs and thus bank loan interest rates (although the latter connection might be loose). Or it can buy bonds: by influencing bond prices, the central bank influences bond yields, and given its monopoly status, the Fed can print up the dollars it needs at any point in time.

Or the Fed can make it clear to investors that it is ready to fight any form of crisis, that it will bail out the system “no matter the cost,” so to speak. Suppose such a promise is considered credible from the financial market community’s point of view. In that case, interest rates and risk premiums will miraculously remain low without any bond purchases on the part of the Fed. And it is by no means an exaggeration to say that putting a safety net under the system has become perhaps the most powerful policy tool in the Fed’s bag of tricks. Largely hidden from the public eye, it allows the Fed to keep the fiat money system afloat.

The critical factor in all this is the interest rate. As the Austrian monetary business cycle theory explains, artificially lowering the interest rate sets a boom in motion, which turns to bust if the interest rate rises. And the longer the central bank succeeds in pushing down the interest rate, the longer it can sustain the boom. This explains why the Fed is so keen to dispel the notion of hiking interest rates any time soon. Tapering would not necessarily result in an immediate upward pressure on interest rates—if investors willingly buy the bonds the Fed is no longer willing to buy, and/or if the bond supply declines.

But is it likely that investors will remain on the buy side? On the one hand, they have a good reason to keep buying bonds: they can be sure that in times of crisis, they will have the opportunity to sell them to the Fed at an attractive price; and that any bond price decline will be short lived, as the Fed will correct it quickly. On the other hand, however, investors demand a positive real interest rate on their investment. Smart money will rush to the exit if nominal interest rates are persistently too low and expected inflation persistently too high. The ensuing sell-off in the bond market would force the Fed to intervene to prevent interest rates from rising.

Otherwise, as noted earlier, rising interest rates would collapse the debt pyramid and result in a collapse in output and employment. It is, therefore, no wonder that the Fed is doing whatever it can to hide the inflationary consequences of its policy from the public: the steep rise in consumer goods price inflation is being dismissed as only “temporary”; asset price inflation is said to be outside the policy mandate, and the impression is given that increases in stock, housing, and real estate prices do not represent inflation. Meanwhile, the increase in the money supply—which is the root cause of goods price inflation—is barely mentioned.

However, once people begin to lose confidence in the Fed’s willingness and ability to keep goods price inflation low, the “safety net trickery” reaches a crossroads. If the Fed then decides to keep interest rates artificially low, it will have to monetize growing amounts of debt and issue ever-larger amounts of money, which, in turn, will drive up goods price inflation and intensify the bond sell-off: a downward spiral begins, leading to a possibly severe devaluation of the currency. If the Fed prioritizes lowering inflation, it must raise interest rates and reign in money supply growth. This will most likely trigger a rather painful recession-depression, potentially the biggest of its kind in history.

Against this backdrop, it is difficult to see how we could escape the debasement of the US dollar and the recession. It is likely that high, perhaps very high, inflation will come first, followed by a deep slump. For inflation is typically seen as the lesser of two evils: rulers and the ruled would rather new money be issued to prevent a crisis over allowing businesses to fail and unemployment to surge dramatically—at least in an environment where people still consider inflation to be relatively low. There is a limit to the central bank’s machinations, though. It is reached when people start distrusting the central bank’s currency and dumping it because they expect goods price inflation to spin out of control.

But until this limit is reached, the central bank still has quite some leeway to continue its inflationary policy and increase the damage: debasing the purchasing power of money, increasing overconsumption and malinvestment, and making big government even bigger, effectively creating a socialist tyranny if not stopped at some point. So, better stop it. If we wish to do so, Ludwig von Mises (1881–1973) tells us how: “The belief that a sound monetary system can once again be attained without making substantial changes in economic policy is a serious error. What is needed first and foremost is to renounce all inflationist fallacies. This renunciation cannot last, however, if it is not firmly grounded on a full and complete divorce of ideology from all imperialist, militarist, protectionist, statist, and socialist ideas."1

Author:

Dr. Thorsten Polleit is Chief Economist of Degussa and Honorary Professor at the University of Bayreuth. He also acts as an investment advisor.

Subscribe to our evening newsletter to stay informed during these challenging times!!